kaiyun开云体育平台-(中国)科技公司,

kaiyun开云体育平台-(中国)科技公司,

欢迎您进入kaiyun开云体育平台-(中国)科技公司,官网!

打造国际一流的工程咨询企业

0571-86588296

0571-86588296

公司简介

Company profile

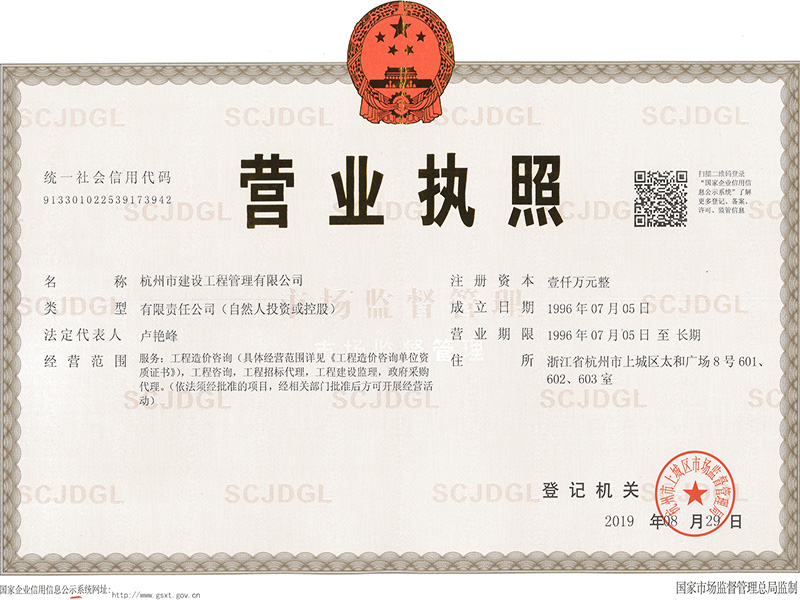

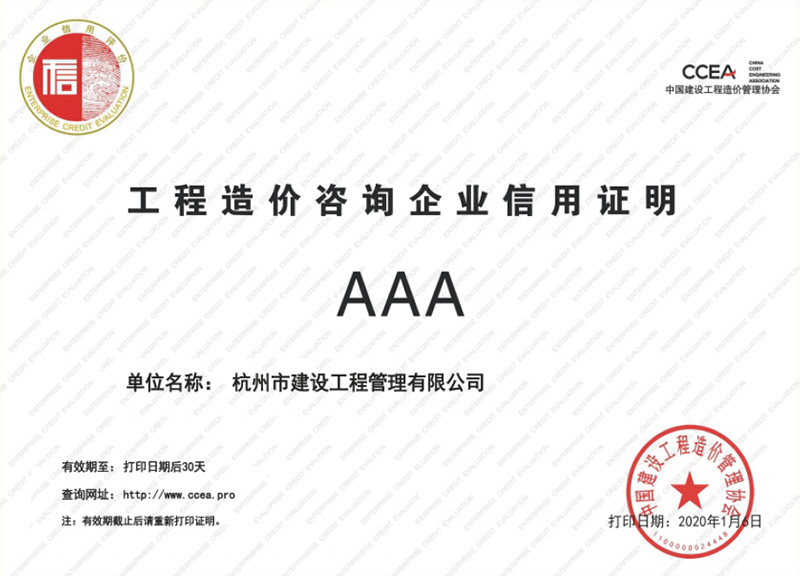

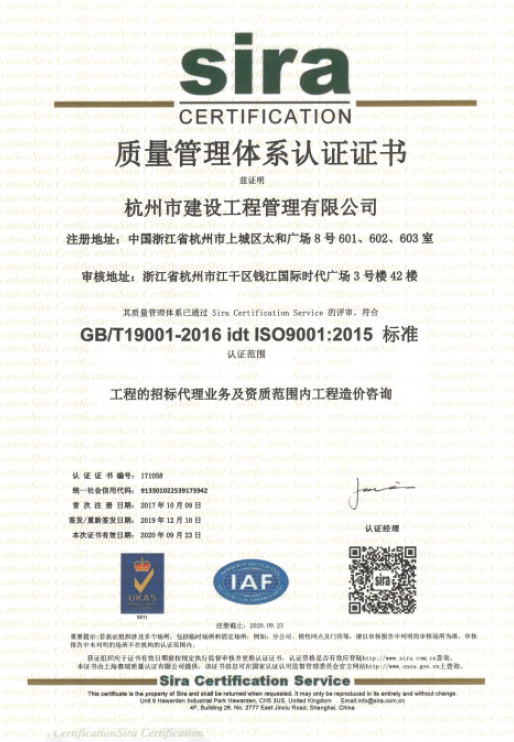

kaiyun开云体育平台-(中国)科技公司,成立于1996年7月,公司原名“杭州市建设工程招标代理有限公司”。原隶属于杭州市建委(杭州市建筑业管理局),是浙江省第一批招标代理、造价咨询企业。为响应政府主管部门的号召,于2000年12月实施了具有历史性的改制工作,完成了独立核算、自主经营的战略转变。2021年,公司正式更名为“kaiyun开云体育平台-(中国)科技公司,”,以全新的面貌、更高的服务质量、更严谨的管理体系为客户提供更为优质的服务。公司在发展的每个阶段都以前瞻的思想……

了解详情>>政府合作

government cooperation

| 省 级: | 浙江省审计厅、浙江省财政厅…… |

| 地市级: | 杭州市审计局、杭州市财政局、温州市财政局、湖州市农业局…… |

| 区县级: | 瑞安市财政局、余姚市农林局、成都市凉山州公路管理局;桐乡市财政局;桐乡市审计局、龙泉市建设局、建德市财政局、浦江县财政局、龙游县民政局、青田县财政局、重庆市奉节财政局,重庆市石柱县财政局,海盐县财政项目预算审核中心;海盐县交通运输局、云和县财政局;杭州市余杭区财政局;杭州市余杭区审计局;杭州市余杭区发展和改革局;杭州市临安区财政局;杭州市临安区审计局;金华市金东区农业农村局;金华市婺城区卫生健康局;金华市金东区卫生健康局;金华市婺城区住房和城乡建设局;金华市金东区教育体育局;杭州市富阳区财政局;杭州市富阳区审计局;杭州市桐庐区财政局;杭州市桐庐区审计局;台州市黄岩区财政局…… |

关注微信

Copyright @ 2020 hzgcgl.com All Rights Reserved. 版权所有:kaiyun开云体育平台-(中国)科技公司, 开创网络 技术支持 网站备案号:浙ICP备11006319号-1